CfD allocation round 6 predictions

Miriam Noonan discusses the announcement by UK Government to increase the strike price caps for the upcoming Contract for Difference (CfD) round.

Miriam Noonan – Commercial Manager

The announcement last week by the UK Government to increase the strike price caps for the upcoming Contract for Difference (CfD) round is good news for floating offshore wind test and demonstration projects like Llŷr 1&2 – it shows the government is listening to the industry and recognises the need to build investor confidence to enable the UK to secure a head start in the global race to develop floating offshore wind.

The administrative strike price for floating offshore wind (FLOW) in Allocation Round 6 (AR6) will be set at £176/MWh[1], up 52% on the £116/MWh in this year’s AR5 tender that did not result in any bids from eligible developers.

Whilst the increased CfD cap is welcome news, there are more parameters at play which are yet to be announced by DESNZ (UK Government Department for Energy Security and Net Zero). It’s also important to remember that we will not know their full generosity until the pot budget is announced, likely in March 2024.

Monetary budget*

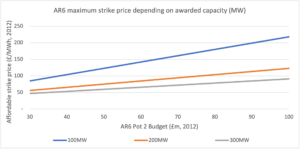

DESNZ sets a total monetary budget for each pot in the Allocation Round. In AR5, the pot two budget was £37m in each delivery year. FLOW shared this pot with advanced conversion technologies, anaerobic digestion (>5MW), dedicated biomass with CHP, geothermal, tidal stream and wave.

At the AR6 strike price cap of £176 per MWh, only 49MW would be affordable at the AR5 budget of £37m. Figure 1shows the impact of the available budget on affordable strike price. For 100MW to be affordable with a pot budget of £37m, a strike price below £95 per MWh is required.

In AR5, a minimum of 10MW tidal was applied within pot two which would have further reduced the available budget. Given the success of tidal in AR5, it is less likely that a ringfence will be applied in AR6.

My expectation is that the pot budget will increase to around £50-60m – a level that could support 100-150MW at a strike price of £120-140 per MWh.

[1] https://assets.publishing.service.gov.uk/media/6555dca8d03a8d000d07fa12/cfd-ar6-administrative-strike-price-methodology.pdf

Market reference price

The allocation of budget is based on the difference between the strike price and the market reference price set by DESNZ to be representative of a long term average wholesale price. In AR5, this was set at £33.56 per MWh in 2028/29 and £27.79 per MWh in 2029/2030.

This is around 35% below the DESNZ reference wholesale market forecast[1] for those years. Although this has had pushback from industry as being too conservative, it may be representative depending on market response to increasing offshore wind capacity as a proportion of total UK generation. Cornwall Insight estimate the capture price of offshore wind at 75.4% of the wholesale price in 2030/31[2].

This parameter is unlikely to significantly change in AR6 but it does present a huge opportunity for storage technologies to capitalise on the price differential between intermittent generation and market demand.

Load factor

DESNZ sets a load factor for each technology which drives the calculation of MWh produced per MW installed to allocate the level of budget taken by a project. In AR5, this was set at 60.4% for FLOW.

This is higher than projects would achieve over a long term and is seen as over-conservative by many in the industry, with the effect that it overestimates the budgetary impact of each MW installed.

This parameter is unlikely to significantly change in AR6.

* Note all values presented are in 2012 terms consistent with CfD announcements unless stated otherwise.

[1] Annex M: https://www.gov.uk/government/publications/energy-and-emissions-projections-2021-to-2040

[2]https://web.archive.org/web/20210816095136/https:/www.cornwall-insight.com/uploads/es%20analysis%20papers/final_1805_wholesale%20power%20price%20cannibalisation.pdf